what happens to the future value of an annuity as the interest rate increases?

The Relationship Between Present and Future Value

Nowadays value (PV) and time to come value (FV) mensurate how much the value of coin has changed over time.

Learning Objectives

Discuss the relationship between present value and time to come value

Key Takeaways

Key Points

- The time to come value (FV) measures the nominal future sum of money that a given sum of coin is "worth" at a specified time in the future assuming a certain interest rate, or more generally, rate of return. The FV is calculated by multiplying the present value past the accumulation function.

- PV and FV vary jointly: when one increases, the other increases, assuming that the interest rate and number of periods remain constant.

- As the interest rate ( discount rate) and number of periods increment, FV increases or PV decreases.

Key Terms

- discounting: The procedure of finding the nowadays value using the discount rate.

- nowadays value: a time to come amount of money that has been discounted to reflect its electric current value, as if it existed today

- capitalization: The procedure of finding the futurity value of a sum by evaluating the present value.

The time to come value (FV) measures the nominal hereafter sum of money that a given sum of money is "worth" at a specified time in the hereafter bold a certain interest rate, or more by and large, rate of render. The FV is calculated by multiplying the nowadays value by the aggregating function. The value does not include corrections for inflation or other factors that bear on the true value of coin in the future. The procedure of finding the FV is often chosen capitalization.

On the other hand, the present value (PV) is the value on a given engagement of a payment or series of payments made at other times. The process of finding the PV from the FV is called discounting .

PV and FV are related, which reflects compounding interest ( unproblematic involvement has n multiplied by i, instead of equally the exponent). Since it'due south really rare to use simple interest, this formula is the important i.

![]()

FV of a unmarried payment: The PV and FV are directly related.

PV and FV vary directly: when one increases, the other increases, assuming that the interest charge per unit and number of periods remain constant.

The interest rate (or disbelieve rate) and the number of periods are the ii other variables that affect the FV and PV. The higher the interest rate, the lower the PV and the higher the FV. The same relationships employ for the number of periods. The more fourth dimension that passes, or the more than interest accrued per period, the higher the FV will be if the PV is constant, and vice versa.

The formula implicitly assumes that in that location is but a unmarried payment. If there are multiple payments, the PV is the sum of the present values of each payment and the FV is the sum of the hereafter values of each payment.

Calculating Perpetuities

The nowadays value of a perpetuity is simply the payment size divided past the interest rate and there is no future value.

Learning Objectives

Calculate the present value of a perpetuity

Key Takeaways

Key Points

- Perpetuities are a special blazon of annuity; a perpetuity is an annuity that has no finish, or a stream of cash payments that continues forever.

- To find the future value of a perpetuity requires having a future appointment, which finer converts the perpetuity to an ordinary annuity until that point.

- Perpetuities with growing payments are called Growing Perpetuities; the growth rate is subtracted from the interest rate in the present value equation.

Primal Terms

- growth rate: The percentage past which the payments abound each period.

Perpetuities are a special type of annuity; a perpetuity is an annuity that has no end, or a stream of cash payments that continues forever. Substantially, they are ordinary annuities, simply have no terminate date. There aren't many actual perpetuities, but the United Kingdom has issued them in the past.

Since there is no end date, the annuity formulas nosotros have explored don't apply here. There is no end date, and then in that location is no future value formula. To find the FV of a perpetuity would require setting a number of periods which would hateful that the perpetuity up to that point can be treated as an ordinary annuity.

There is, however, a PV formula for perpetuities. The PV is simply the payment size (A) divided by the interest rate (r). Notice that at that place is no northward, or number of periods. More accurately, is what results when you lot accept the limit of the ordinary annuity PV formula every bit due north → ∞.

It is too possible that an annuity has payments that grow at a certain charge per unit per period. The charge per unit at which the payments change is fittingly chosen the growth rate (k). The PV of a growing perpetuity is represented equally [latex]\text{PVGP} \ = \ {\text{A} \over ( \text{i} - \text{one thousand} )}[/latex]. It is essentially the same as in except that the growth rate is subtracted from the involvement charge per unit. Another way to recall about it is that for a normal perpetuity, the growth rate is just 0, then the formula boils down to the payment size divided by r.

Calculating Values for Different Durations of Compounding Periods

Finding the Effective Almanac Rate (EAR) accounts for compounding during the twelvemonth, and is easily adjusted to different menstruum durations.

Learning Objectives

Calculate the nowadays and futurity value of something that has dissimilar compounding periods

Central Takeaways

Cardinal Points

- The units of the flow (e.yard. ane year) must exist the aforementioned as the units in the interest rate (e.k. seven% per year).

- When interest compounds more than once a year, the constructive interest charge per unit (EAR) is different from the nominal interest rate.

- The equation in skips the step of solving for EAR, and is directly usable to discover the nowadays or future value of a sum.

Fundamental Terms

- present value: Also known as present discounted value, is the value on a given date of a payment or series of payments made at other times. If the payments are in the hereafter, they are discounted to reverberate the time value of money and other factors such equally investment run a risk. If they are in the past, their value is correspondingly enhanced to reflect that those payments have been (or could accept been) earning interest in the intervening time. Present value calculations are widely used in business and economics to provide a means to compare cash flows at different times on a meaningful "like to like" basis.

- Future Value: The value of an asset at a specific date. It measures the nominal futurity sum of money that a given sum of money is "worth" at a specified time in the future, bold a certain interest charge per unit, or more than generally, charge per unit of return, information technology is the present value multiplied past the aggregating role.

Sometimes, the units of the number of periods does not lucifer the units in the interest rate. For example, the interest rate could be 12% compounded monthly, simply one catamenia is ane year. Since the units accept to be consistent to discover the PV or FV, you could change one period to one month. Merely suppose you lot want to catechumen the interest rate into an annual charge per unit. Since involvement generally compounds, information technology is not equally simple as multiplying 1% by 12 (1% compounded each calendar month). This atom will discuss how to handle different compounding periods.

Effective Annual Rate

The effective annual charge per unit (EAR) is a measurement of how much involvement actually accrues per year if it compounds more than than in one case per twelvemonth. The EAR tin can be establish through the formula in where i is the nominal interest rate and n is the number of times the interest compounds per year (for continuous compounding, encounter ). Once the EAR is solved, that becomes the involvement rate that is used in any of the capitalization or discounting formulas.

![]()

EAR with Continuous Compounding: The constructive rate when interest compounds continuously.

![]()

Calculating the effective annual rate: The constructive annual rate for interest that compounds more than once per year.

For example, if there is 8% interest that compounds quarterly, you plug.08 in for i and 4 in for north. That calculates an EAR of.0824 or eight.24%. You can recall of it as 2% interest accruing every quarter, simply since the interest compounds, the amount of interest that actually accrues is slightly more than 8%. If you wanted to detect the FV of a sum of money, you would have to utilize 8.24% not viii%.

Solving for Nowadays and Future Values with Different Compounding Periods

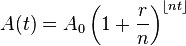

Solving for the EAR and then using that number as the effective interest rate in present and future value (PV/FV) calculations is demonstrated hither. Luckily, it'southward possible to contain compounding periods into the standard time-value of money formula. The equation in is the same as the formulas we accept used before, except with different annotation. In this equation, A(t) corresponds to FV, A0 corresponds to Present Value, r is the nominal involvement charge per unit, n is the number of compounding periods per year, and t is the number of years.

FV Periodic Compounding: Finding the FV (A(t)) given the PV (Ao), nominal interest rate (r), number of compounding periods per year (n), and number of years (t).

The equation follows the aforementioned logic every bit the standard formula. r/northward is only the nominal interest per compounding period, and nt represents the total number of compounding periods.

Solving for north

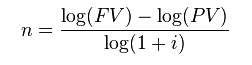

The last tricky office of using these formulas is figuring out how many periods in that location are. If PV, FV, and the interest charge per unit are known, solving for the number of periods tin be catchy because n is in the exponent. Information technology makes solving for northward manually messy. shows an easy way to solve for n. Call back that the units are of import: the units on n must exist consistent with the units of the interest rate (i).

Solving for northward: This formula allows you to figure out how many periods are needed to accomplish a certain future value, given a present value and an interest rate.

Comparing Interest Rates

Variables, such every bit compounding, inflation, and the cost of capital must be considered before comparing involvement rates.

Learning Objectives

Hash out the differences between effective interest rates, real interest rates, and cost of majuscule

Cardinal Takeaways

Central Points

- A nominal interest charge per unit that compounds has a different constructive rate (EAR), because interest is accrued on involvement.

- The Fisher Equation approximates the amount of involvement accrued after bookkeeping for inflation.

- A company will theoretically only invest if the expected render is college than their cost of upper-case letter, even if the render has a loftier nominal value.

Fundamental Terms

- aggrandizement: An increase in the general level of prices or in the cost of living.

The corporeality of interest you would have to pay on a loan or would earn on an investment is clearly an important consideration when making any financial decisions. However, it is non enough to simply compare the nominal values of two involvement rates to meet which is college.

Effective Interest Rates

The reason why the nominal interest rate is merely part of the story is due to compounding. Since interest compounds, the amount of interest really accrued may be different than the nominal amount. The last section went through one method for finding the amount of interest that actually accrues: the Constructive Annual Rate (EAR).

The EAR is a calculation that business relationship for interest that compounds more than than i time per twelvemonth. It provides an annual involvement rate that accounts for compounded involvement during the year. If two investments are otherwise identical, you would naturally pick the 1 with the higher EAR, fifty-fifty if the nominal rate is lower.

Real Interest Rates

Interest rates are charged for a number of reasons, but one is to ensure that the creditor lowers his or her exposure to aggrandizement. Inflation causes a nominal amount of money in the present to accept less purchasing power in the hereafter. Expected inflation rates are an integral office of determining whether or not an involvement rate is loftier enough for the creditor.

The Fisher Equation is a unproblematic way of determining the existent involvement rate, or the interest charge per unit accrued afterwards accounting for aggrandizement. To find the existent interest rate, simply decrease the expected aggrandizement rate from the nominal interest rate.

![]()

Fisher Equation: The nominal involvement rate is approximately the sum of the real interest charge per unit and inflation.

For example, suppose y'all take the option of choosing to invest in two companies. Company 1 will pay y'all v% per year, but is in a country with an expected aggrandizement rate of iv% per year. Company 2 will but pay 3% per twelvemonth, but is in a country with an expected inflation of i% per twelvemonth. By the Fisher Equation, the real interest rates are i% and two% for Company one and Company 2, respectively. Thus, Company two is the improve investment, even though Visitor 1 pays a higher nominal interest rate.

Cost of Uppercase

Another major consideration is whether or not the involvement rate is higher than your cost of upper-case letter. The toll of capital is the charge per unit of return that capital could exist expected to earn in an culling investment of equivalent run a risk. Many companies have a standard cost of capital that they utilise to make up one's mind whether or non an investment is worthwhile.

In theory, a company will never make an investment if the expected return on the investment is less than their toll of capital letter. Even if a 10% annual return sounds really overnice, a company with a 13% cost of capital volition not make that investment.

Calculating Values for Fractional Time Periods

The value of coin and the balance of the account may be unlike when considering fractional time periods.

Learning Objectives

Summate the hereafter and present value of an account when a fraction of a compounding period has passed

Key Takeaways

Fundamental Points

- The balance of an account only changes when interest is paid. To detect the residue, round the partial fourth dimension menses down to the period when involvement was last accrued.

- To find the PV or FV, ignore when involvement was last paid an use the partial time menses equally the fourth dimension period in the equation.

- The discount rate is really the cost of non having the money over fourth dimension, so for PV/FV calculations, it doesn't matter if the involvement hasn't been added to the account nevertheless.

Key Terms

- time period supposition: business profit or loses are measured on timely basis

- compounding period: The length of time between the points at which interest is paid.

- fourth dimension value of money: the value of an asset accounting for a given amount of involvement earned or inflation accrued over a given flow

Up to this point, we have implicitly assumed that the number of periods in question matches to a multiple of the compounding period. That means that the point in the future is also a point where involvement accrues. But what happens if we are dealing with fractional time periods?

Compounding periods can be whatever length of time, and the length of the menstruum affects the rate at which involvement accrues.

Compounding Interest: The consequence of earning 20% almanac interest on an initial $i,000 investment at various compounding frequencies.

Suppose the compounding period is one twelvemonth, starting January1, 2012. If the trouble asks you to find the value at June 1, 2014, at that place is a bit of a conundrum. The terminal time involvement was really paid was at Jan 1, 2014, but the fourth dimension-value of money theory clearly suggests that it should be worth more than in June than in Jan.

In the case of fractional time periods, the devil is in the details. The question could inquire for the time to come value, present value, etc., or it could ask for the future residuum, which accept different answers.

Future/Present Value

If the problem asks for the future value (FV) or present value (PV), information technology doesn't really matter that you are dealing with a fractional time period. You can plug in a fractional fourth dimension period to the appropriate equation to observe the FV or PV. The reasoning behind this is that the interest rate in the equation isn't exactly the interest rate that is earned on the money. It is the same as that number, simply more broadly, is the toll of not having the money for a time catamenia. Since there is still a cost to not having the money for that fraction of a compounding menstruum, the FV notwithstanding rises.

Business relationship Balance

The question could alternatively ask for the remainder of the account. In this case, you need to find the corporeality of money that is actually in the account, so y'all round the number of periods down to the nearest whole number (assuming i period is the same as a compounding period; if not, circular downwardly to the nearest compounding period). Fifty-fifty if interest compounds every period, and you are asked to find the balance at the 6.9999th period, you need to round down to 6. The last time the account really accrued interest was at period 6; the involvement for period seven has not still been paid.

If the account accrues involvement continuously, at that place is no problem: there can't be a partial fourth dimension menstruum, so the balance of the account is always exactly the value of the coin.

Loans and Loan Amortization

When borrowing money to be paid back via a number of installments over fourth dimension, information technology is important to understand the time value of coin and how to build an amortization schedule.

Learning Objectives

Understand acquittal schedules

Cardinal Takeaways

Key Points

- Acquittal of a loan is the process of identifying a payment amount for each period of repayment on a given outstanding debt.

- Repaying capital over fourth dimension at an involvement rate requires an acquittal schedule, which both parties agree to prior to the exchange of capital. This schedule determines the repayment period, as well as the amount of repayment per period.

- Fourth dimension value of money is a central concept to acquittal. A dollar today, for example, is worth more than than a dollar tomorrow due to the opportunity cost of other investments.

- When purchasing a home for $100,000 over 30 years at 8% interest (consistent payments each month), for example, the total amount of repayment is more than 2.5 times the original principal of $100,000.

Key Terms

- amortization: This is the process of scheduling intervals of payment over fourth dimension to pay back an existing debt, taking into account the time value of money.

When lending money (or borrowing, depending on your perspective), information technology is mutual to have multiple payback periods over time (i.e. multiple, smaller cash menstruation installments to pay back the larger borrowed sum). In these situations, an acquittal schedule will be created. This will determine how much will exist paid back each catamenia, and how many periods of repayment will be required to cover the principal residual. This must be agreed upon prior to the initial borrowing occurs, and signed by both parties.

Time Value of Money

Now if y'all add up all of the separate payments in an acquittal schedule, you'll find the total exceeds the amount borrowed. This is considering amortization schedules must take into account the time value of money. Time value of coin is a fairly uncomplicated concept at information technology'due south core: a dollar today is worth more than a dollar tomorrow.

Why? Because capital tin can be invested, and those investments tin yield returns. Lending your coin to someone means incurring the opportunity cost of the other things you could do with that coin. This gets even more drastic equally the scale of capital increases, as the returns on upper-case letter over time are expressed in a percentage of the capital invested. Say you spend $100 on some stock, and turn 10% on that investment. You now have $110, a profit of $10. Say instead of simply a $100, yous put in $10,000. Now you have $11,000, a profit of $1,000.

Principle and Interest

As a result of this calculation, amortization schedules charge interest over time as a percentage of the principal borrowed. The calculation will contain the number of payment periods (n), the principal (P), the acquittal payment (A) and the interest rate (r).

[latex]{\displaystyle \text{P}\,=\,\text{A}\cdot {\frac {1-\left({\frac {1}{one+\text{r}}}\correct)^{\text{north}}}{\text{r}}}}[/latex]

To brand this a fleck more realistic, let'south insert some numbers. Let'southward say you observe a dream house, at the reasonable rate of $100,000. Unfortunately, a scrap of irresponsible borrowing in your by ways you must pay 8% interest over a 30 yr loan, which volition be paid via a monthly amortization schedule (12 months x xxx years = 360 payments total). If you do the math, you should notice yourself paying $734 per month 360 times. 360 ten 734 will exit you lot in the ballpark of $264,000 in total repayment. that means you are paying more than ii.v times equally much for this house due to time value of money! This bit of knowledge is absolutely disquisitional for personal financial decisions, every bit well as for high level business organisation decisions.

Amortization Schedule Example: This shows the start few installments in the example discussed above (i.e. borrowing $100,000 at 8% interest paid monthly over xxx years).

Source: https://courses.lumenlearning.com/boundless-finance/chapter/additional-detail-on-present-and-future-values/

0 Response to "what happens to the future value of an annuity as the interest rate increases?"

Post a Comment